Must-read blogs

- Casinos Not On Gamstop

- Casino Con Bonus Di Benvenuto

- UK Online Casinos Not On Gamstop

- Migliori Bookmakers Non Aams

- Gambling Sites Not On Gamstop

- Non Gamstop Casinos UK

- Non Gamstop Casino UK

- Slots Not On Gamstop

- Best Non Gamstop Casinos

- Sites Not On Gamstop

- Non Gamstop Casino

- Sites Not On Gamstop

- Slots Not On Gamstop

- UK Casino Not On Gamstop

- Casino Non Aams

- Best UK Online Casino Sites

- Migliori Siti Di Scommesse

- Sites Not On Gamstop

- Casino En Ligne Fiable

- Non Gamstop Casino UK

- Non Gamstop Casino

- Non Gamstop Casinos

- Non Gamstop Casino

- Migliori Casino Online Italiani

- Best Betting Sites Not On Gamstop

- Meilleur Casino Crypto

- Sites De Paris Sportifs Belgique

- Casino En Ligne Fiable

- найкращі крипто казино

- Meilleur Casino Sans Kyc

- Casino Cresus

- Bonus Gratuit Sans Dépôt

- Casino Senza KYC

- Meilleur Casino En Ligne

- Migliori Crypto Casino

- Meilleur Site Casino En Ligne Belgique

- Casino En Ligne Argent Réel

- Casino En Ligne Français

- Meilleur Casino En Ligne France

- Migliori Siti Poker Online

- Casino En Ligne France

- Migliori App Per Giocare A Poker

- Casino En Ligne Retrait Instantané

Sunday Train has covered the California HSR project on a number of occasions in the past. However, there was no special attention given to what was widely covered at the time as the "end of California HSR", when a judge ruled that the proposed Business Plan did not meet the terms of the Prop1A(2008) which governed the sale of much of the $9m in state bond authority which had passed in 2008. The Sacramento Bee covered the issue at the time, including the appeal of the ruling to the Supreme Court.

Sunday Train has covered the California HSR project on a number of occasions in the past. However, there was no special attention given to what was widely covered at the time as the "end of California HSR", when a judge ruled that the proposed Business Plan did not meet the terms of the Prop1A(2008) which governed the sale of much of the $9m in state bond authority which had passed in 2008. The Sacramento Bee covered the issue at the time, including the appeal of the ruling to the Supreme Court.

And the reason the Sunday Train did not cover that court judgement is IANDL (I Aint No Dang Lawyer), so I was waiting to see what actually happened with respect to funding for the project. And now it appears to me that funding for the original segment from north of Fresno to the outskirts of Bakersfield has been secured, with the news that part of the Budget deal has secured Cap and Trade funding for the HSR project.

More on what this means, below the fold.

Funding Construction & Operating Segments and All That

OK, first, what was the economics behind the legal issue the California HSR Authority (CHSRA) was facing? Its the basic threshold problem for intercity passenger rail. It is feasible for "bullet train" HSR (conventionally a train operating faster than 125mph, though the first "bullet trains" were actually 100mph) operating on a wide range of intercity corridors to get sufficient patronage to run without operating subsidies.

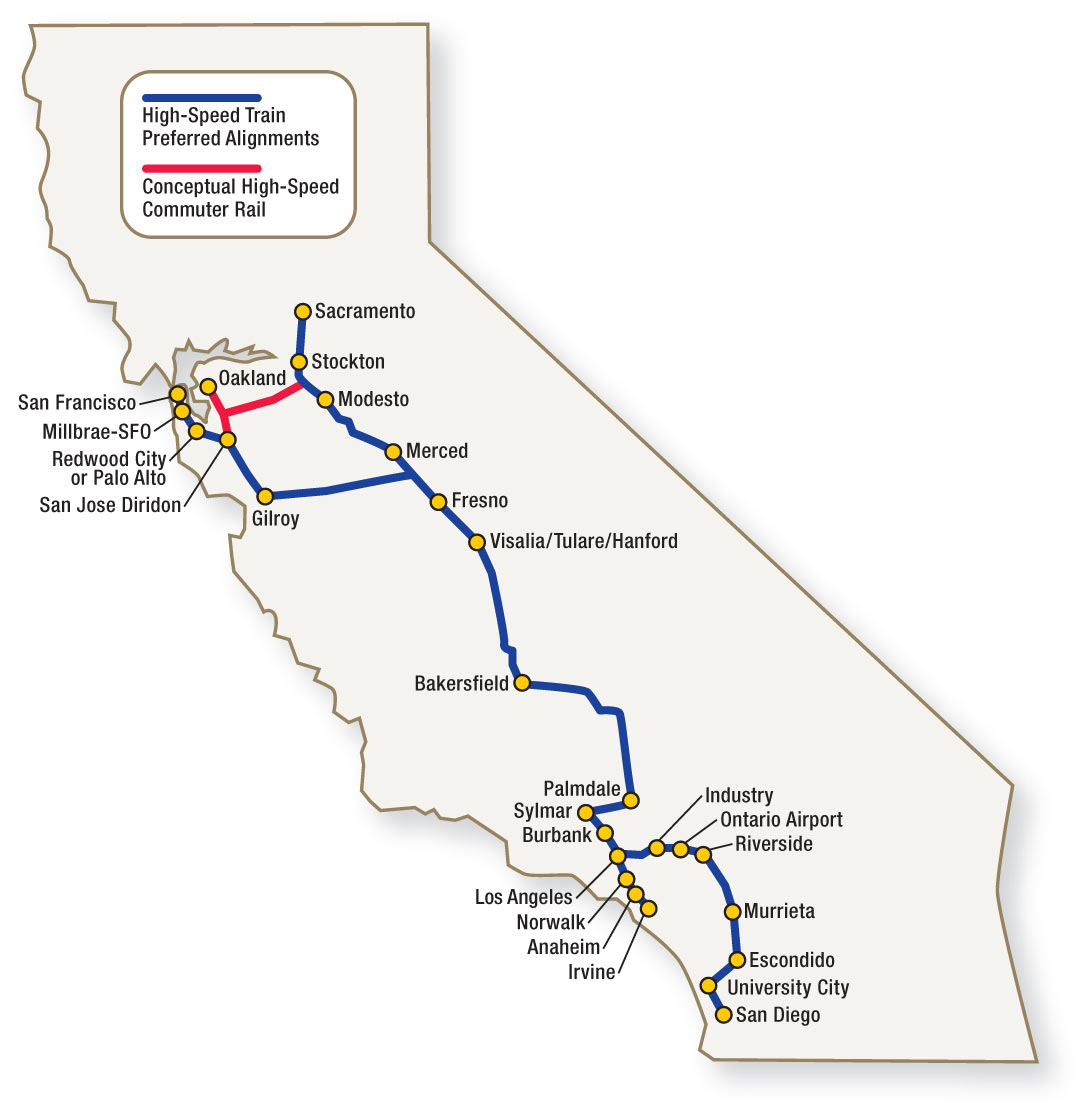

However, that is not for just any alignment. That is so long as there is sufficient population along the corridor and so long as at least one end has a sufficiently strong anchor. In the California context, that translates into viable HSR corridors from San Diego to LA, LA through Fresno in the San Joaquin Valley, San Francisco through to Bakersfield in the San Joaquin Valley, and San Francisco through to Sacramento.

And so when you look at the planned California HSR alignment, what do you see? A "double Y" formation supporting LA / San Diego, LA / SF via the San Joaquin Valley, LA / Sacramento via the San Joaquin Valley and a supplementary connector for SF / Sacramento.

And so when you look at the planned California HSR alignment, what do you see? A "double Y" formation supporting LA / San Diego, LA / SF via the San Joaquin Valley, LA / Sacramento via the San Joaquin Valley and a supplementary connector for SF / Sacramento.

The threshold problem is that the first phase is the LA Basin to Bay Area part of the route matrix connected via the San Jaoquin Valley backbone, and both the LA Basin and Bay Area have difficult geography to get through to connect to the San Joaquin Valley backbone.

And this becomes a legal issue because the Prop1A(2008) to provide $9b in bond funding for HSR (and some extra for complementary rail transport) includes a range of measures to protect the bond authority from being raided. In particular, it was supposed to be protected from being used to provide capital subsidies to subsidized commuter rail service, or subsidized Amtrak California intercity rail services. It was supposed to be for "genuine HSR", and the demand that it run without operating subsidy is one that a well-designed HSR system can readily meet, but which commuter rail or conventional intercity rail would struggle to meet.

Prop1A(2008) was passed on the ballot in the same election that saw President Obama elected, and it was shortly after that the one-off $8b in HSR funding was included in the Stimulus II legislation, the "ARRA". Then-Governor Schwarzenegger applied for HSR funding, promising a 50:50 state match ~ the highest level of state match allowed under Prop1A(2008).

That was, of course, a reckless decision, since there was no way to run a self-supporting service on the Construction Segment originally awarded from a bit north of Fresno to a bit south, and even after that initial Construction Segment was extended, it still was not enough to offer a self-sustaining service on that Initial Construction Segment alone.

The reason that the FRA is willing to fund a partial operating segment is that California already has passenger rail in the San Joaquin Valley, the Amtrak-CA San Jaoquin, running three times a day each way. So the FRA was willing to fund an "Initial Construction Segment" on the promise of a down payment on building an HSR system which, at the same time, could as a back-up contingency be used to substantially upgrade the Amtrak-CA service.

But that is a Federal Rule about "independent utility" when funding parts of a corridor. Prop1A(2008) don't care about no "independent utility": it specifies a self-sustaining Initial Operating Service to authorize release of the bulk of Prop1A(2008) bonds.

And the CHSRA Business Plan seemed to be "we'll seek additional Federal and State funding to fund building the balance of the Initial Operating Service, once this Initial Construction Segment is completed." Which, from what I understand (though, remember, IANDL), is what the court ruling said wasn't good enough.

To be specific, their projected cumulative cost for an Initial Operating Service, from north of Fresno to the somewhere in the general area of Burbank in the San Fernando Valley in the LA Basin, is about $31b. That's the threshold test for the Prop1A(2008) funding ~ except for an amount allowed to be used for preliminary program costs, most of the bonds are under a condition of a Business Plan for establishing a service that can be run without operating subsidies.

However, the Initial Construction Segment has a cost of $6b, with $3.3b coming from Federal funding and $2.6b in Prop1A(2008) bond funding. So while the legal fight is over the $31b in Initial Operating Service project cost, the "breaking ground" fight is over $2.4b in state funding to match $3.3b in already authorized, appropriated, and awarded Federal funds. And it is that fight which appears to be settled with this deal.

Funding HSR from Cap and Trade funds

The Sunday Train has addressed the issue of funding HSR with cap and trade funds, back in April of 2012, well before the court ruling threw the project into a state of uncertainty at the beginning of this year. I reprinted that essay in March of this year, under the title: Sunday Train: Cap&Trade Funds should help finance the California HSR. So I don't suppose there is much ground for uncertainty on where I stand on Cap and Trade funds helping to finance the California HSR project

To summarize, the issue raised by critics of the use of Cap & Trade funds for capital subsidy for an HSR project is the efficiency of the use of funds. The argument is that the Cap & Trade funds should be devoted to projects with the greatest "bang for the buck" in terms of reducing GHG emissions.

The first issue with this is defining what the "bang" is for projects that serve multiple goals. If, overall, Cap & Trade funds provide 20% of the funding for a project, and that project is being funded from other sources in service of other goals, then in effect you get 100% of the "bang" for only 20% of the project cost "bucks".

So if the "full cost" of emissions reduction is, say, $250/ton, then the effective cost is $50/ton in the example (20% of $250) ... and could range from $25/ton if Cap & Trade funds contribute 10% of the budget, up to $125/ton if Cap & Trade funds contributed a whopping 50% of the budget for a multi-purpose project.

Or, working from a different direction, if the "full cost" of GHG emissions is five times the amount you can justify, then the GHG reduction funding should not fund more than one-fifth of the project cost.

That leads to the second issue, which is setting the target emissions reduction for a project to receive funding. Unless we do enough to avoid climate catastrophe at the level of the collapse of our nation's ability to function as a coherent national society and economy, then the efficiency of the investments we do make is basically pointless.

If we collect together all the most efficient ways of reducing CO2 and doing "enough" requires a carbon price of $60/ton, then that sets our threshold efficiency for a long term project. If "doing enough" requires a carbon price of $90/ton, then that sets our threshold efficiency for a long term project. As described in that piece, given estimates in that range, I settle halfway in the middle at a notional carbon price threshold of $75/ton.

The objection that will be raised by the kind of short-sighted, blinkered analysis performed by the California Legislative Analyst Office is that the Cap and Trade fund can find plenty of investments that are more efficient than that. But that is on a false specification of "plenty". Plenty to exhaust the Cap and Trade funding, to be sure. But not plenty to avoid climate catastrophe.

Simply focusing on getting the maximum efficiency in the context of not doing enough to solve the problem is refusing to make long-term fixes because short-term band-aids are quicker and cheaper.

On Those Grounds, Does The Budget Deal Pass Muster?

So, lets run the numbers. The California HSR is projected to be a $68b project:

- which will have a full-cost price of CO2 reduction of $250/ton to $400/ton.

- At an allowed $75/ton for the CO2 reduction,

- that means that the Cap and Trade funds should be allowed to fund from 18.75% to 30% of the budget cost, or

- Cap and Trade should be allowed to fund $12.7b to $20.4b of the project.

The proposal to use 25% of the Cap and Trade funds is expected to generate $750m to $1b annually, so taking the $12b more conservative estimate of ridership and corresponding CO2 reductions, that is from 12 to 17 years of funding at the estimated $750m to $1b annually.

The funds required to build the Initial Construction Segment are $2.4b, which is 3.6% of the total project cost. So assuming $400/ton at full cost from CO2 funding, just using Cap & Trade funds for that segment alone would have an effective cost of $15/ton.

And so the budget deal means that the Initial Construction Segment can go ahead. $750m to $1b per year from its share of Cap and Trade funds is ample to either fund on a current basis or finance through borrowing $2.4b.

How much more it should fund ... well, since we will know more by the time the question arises, that gets into the fact that The Future's Uncertain (but the End Is Always Near).

What if the Future Is Uncertain

I remember getting a research paper on time on a topic in Intermediate Macroeconomics in which the student was talking about the Post Keynesians. The Post Keynesians lay great stress on the fact that we don't just face risks in financial markets, we face genuine intrinsic uncertainty. "Risk" is like the odds of rolling a six with a balanced six-sided die. True "uncertainty" is like the odds of rolling a six when you don't know whether the person is holding a six sided, ten-sided, twenty-sided or four sided die, and you don't know how interested the person is in actuall rolling the die anyway.

And the first sentence of the student's paper was, "Among all the uncertain things in the world, the future surely ranks near the top of the list."

So, what about uncertainty?

What if we are in reality facing a future in in which an effective carbon price of under $15/ton is enough to get the job done?

Well, that is a future in which we are much wealthier than present information suggests that we will be, and the wealthier we are in a given future scenario, the less of a problem it is to spend money on GHG emissions reduction in a less than perfectly efficient way.

It is if we are facing a future in which the required effective carbon price is much higher than we now expect that it becomes crucial to not "waste" our carbon reduction funds, and in that future, putting $12b to $20b of Carbon Emissions Reduction funding toward HSR is a quite sensible use of CO2 emissions reduction funding.

What if there is no more Federal Funding coming?

This is the kind of issue that was the challenge in releasing Prop1A(2008) bond funds. The Business Plan assumes over 50% of funding from Federal sources. What if there are no Federal sources?

But this is where funding the state match for the Initial Operating Segment out of Cap & Trade funds is such a strategic step forward. Governor Schwarzennegger was truly reckless in promising to use so much of the Prop1A(2008) bond funding at a 50:50 match. For one thing, the Stimulus II HSR funding did not actually require matching funds, since it was part of a Stimulus package and during an economic crisis, state governments are often in a cash crunch. But even for normal Federal funding of intercity-distance passenger transport, an 80:20 Federal:Local match is more common, and for some Interstate spending its a 90:10 match.

Look at the projected $31b cost for the Initial Operating segment. Suppose the $6b for the Initial Construction Segment is not financed with Prop1A(2008) funds. And suppose that $3b are equipment costs that are financed privately by the operator that wins the franchise to operate the service. That leaves $22b to cover.

At an 80:20 match, $22b would call for a $4.4b state contribution ~ well within the reach of the Prop1A(2008) bond authorization.

Which gives a strategy for addressing the uncertainty of Federal Funding. First, build the Initial Construction Segment. That will not be finished after the end of the current administration, so the current House refusal to fund HSR as a refusal to allow President Obama a "win" will no longer be a political issue.

And then freaking win the Federal Funding. This is not forecasting volcanic eruptions or the sunspot cycle we are talking about. This is political decision making in the halls of Congress. When there is an opening to win an adequate level of Federal Funding to allow the Initial Operating Service to be funded ... take it and get it funded.

Normally the advice would be to use bond authorizations, rather than holding them in reserve, because bond authorizations are in "face value" dollar amounts, and inflation eats away at their buying power over time. However, because of Gov. Schwarzennegger's reckless promise of a 50% state match, that's not true in this case. In this case, it makes sense to use current state revenues to fund the State Match of the relatively inexpensive per-mile Initial Construction Segment, and keep the bond authorization in reserve to use with better leverage, to try to fund the more expensive project of getting an effective HSR corridor down into the LA Basin.

What if that fight is lost?

If we cannot ever win a fight in getting Federal funding for useful investment in sustainably powered intercity transport ... well, in that scenario we're probably not going to survive as a coherent national economy or national society.

If we cannot ever win a fight in getting Federal funding for useful investment in sustainably powered intercity transport ... well, in that scenario we're probably not going to survive as a coherent national economy or national society.

And if California or the West Coast is trying to make it on its own, every bit of high quality legacy infrastructure that it can power with sustainable, renewable energy from West Coast Solar, Wind and other sustainable, renewable resources is going to be that much more valuable.

In the future where we lose the fight to get our national government to take steps to defend our country from the catastrophic consequences of our own current action, there will be no regret at all in that future California for any investment in sustainable transport that it inherits.

Conclusions and Conversations

As always, any topic in sustainable transport is on-topic in the Sunday Train. So feel free to take about CO2 emissions reduction, energy independence, suburban retrofit and reversing the cancer of sprawl over our diverse ecosystems, or the latest iPhone or Android app to map you bike ride. Whatever.

The Sunday Train doesn't really leave the station until you jump in and join the conversation so ... All Aboard!

Comments

"The Future Is Right Up There At The Top Of The List"